Overview of Private Credit

Private credit has surged as a pivotal force in financial markets, particularly post-2008 financial crisis, boasting substantial growth in assets under management (AUM) of closed-ended private credit funds, skyrocketing from approximately $500 billion in 2015 to over $2.0 trillion by May of 2024, with projections indicating a potential surge to over $3.5 trillion by the end of the decade. This surge is significantly propelled by regulatory changes, including Basel III and the Dodd-Frank Act, which have tightened capital standards for traditional bank lending. Consequently, banks have curtailed lending activities, creating a ripe environment for private credit providers to flourish.

A significant feature of private credit lies in its minimal correlation with public markets, rendering it an attractive option for investors seeking diversification, particularly amidst economic uncertainty. Furthermore, private credit investments often offer security through collateral and tangible borrower assets, further fortifying investor confidence in this asset class.

The advent of platforms such as Credbull represents a seismic shift in the accessibility of private credit investments. Leveraging blockchain technology and decentralized finance (DeFi) principles, Credbull aims to democratize access to the private credit market, traditionally dominated by institutional investors and High Net Worth individuals. This democratization has the potential to unlock new opportunities for a broader range of investors, catalyzing continued growth and innovation within the private credit landscape.

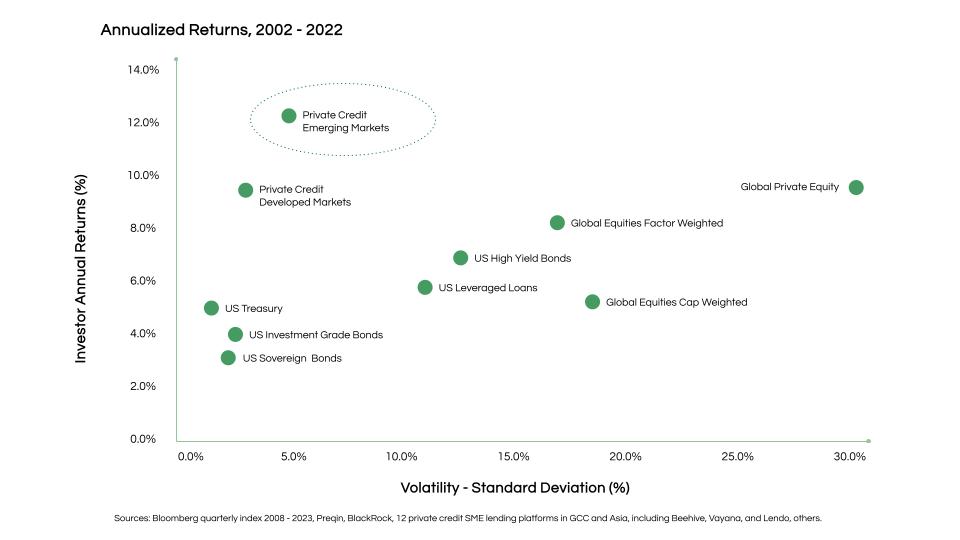

Fig 1: Private Credit in Emerging Markets as the best performing asset class (risk-adjusted).

The Allure of Private Credit's Risk-Return Profile

Private credit presents a "Goldilocks" risk-return profile, striking a balance between risk and reward. Over the past 20 years, it has consistently outperformed traditional fixed-income instruments by an average of approximately 450-500 basis points. This resilience is particularly noteworthy when compared to the volatility of the stock market. For instance, in 2023, the S&P 500 delivered a notable 20% return primarily driven by a surge in just seven tech stocks, leading to inflated P/E ratios. Historical data cautions that such elevated P/E multiples often signal prolonged periods of subdued market performance.

Recognizing the allure of private credit, traditional asset managers have swiftly integrated it into their investment strategies to counter the increasing dominance of passive fund management. This trend is underscored by the participation of major players such as Brookfield, Blackstone, KKR, Apollo, and Ares. In the past two years alone, at least 26 traditional asset managers have either acquired or launched private credit units. This strategic shift underscores private credit's role as a means of capturing superior market returns in an environment marked by growing competition and evolving investment dynamics.

The Growth of Private Credit in Emerging Markets (EMs)

Private credit has emerged as a vital component of the capital structure in emerging markets (EMs), addressing the financing needs of underserved sectors such as energy, agriculture, and infrastructure, which are crucial for economic development. Despite its relatively smaller size compared to developed markets (DMs), annual fundraising for EM private credit has witnessed remarkable growth over the past 15 years, surging from $2.4 billion in 2009 to $12 billion in 2023, marking a 500% increase. Notably, even amidst the challenges posed by COVID-19, 2022 stood out as the second-highest fundraising year since 2008, with significant momentum observed across Asia, the Middle East, Latin America, Africa, and Central & Eastern Europe. India, in particular, is poised for substantial growth, with its private credit market projected to reach $89 billion by 2026, in line with the country’s anticipated GDP growth of 6-7% annually by 2026.

Looking ahead, EMs are expected to outpace DMs in growth, driven by several key factors. Firstly, private credit providers in EMs offer investors compelling propositions, from direct SME lending to asset allocation strategies, providing stability during market volatility, attractive risk-adjusted returns, and robust diversification opportunities. Secondly, as the private credit industry in EMs matures, knowledgeable fund managers with observable track records enhance transparency and investor confidence, facilitating sector growth. Thirdly, long-term structural shifts such as demographic trends, reduced supply-side constraints, industrialization, ongoing reforms, and infrastructure development provide a conducive environment for private credit growth in EMs.

Regulatory changes also play a pivotal role in supporting the maturation of EM private credit markets. Improvements in creditor rights regimes, collateral systems, enforcement mechanisms, and insolvency laws contribute to a more robust and investor-friendly environment. Regulatory advancements, such as SEBI's approval in January 2022 for alternative investment funds to participate in credit default swap transactions in India, further enhance risk management associated with the bond market, fostering investor confidence and sector growth in EM private credit.

The expansion of private credit in emerging markets represents a significant evolution, reflecting the sector's adaptability and essential role in fostering economic growth. As EMs continue to develop and reform, the private credit market is set to play an increasingly prominent role in providing capital, driving innovation, and supporting sustainable development across these dynamic regions.

Updated 3 months ago